Listening to the wrong people

If you ask most people what to do with your career, they’ll tell you to play it safe and stay in that mid-level job with 8% annual salary increases. It’s not that they don’t mean well. It’s just that they’re risk adverse themselves, and they’re probably reluctant to advise you to take the risks you need to for a seven figure income. Listen to your gut, and take those risks. If you do want some solid advice, talk to a millionaire.

Spending more money every year you get a raise

It makes sense to buy that new car and take your girlfriend out to dinner four times a week because you’re making more money, right? Wrong. Save the money you’re making and start investing in stocks or increase your 401K contributions. Sure, you can reward yourself for your hard work every once in a while, but not saving (and investing) a good portion of your paycheck in your 20s can cost you in your 30s and beyond.

Ever watch a show like Shark Tank and wonder where did that guy $100,000 of his own money to invest in his idea? He lived below his means and saved his money so that when the time came to make a move he could. You should too.

Giving up and playing it safe when you fail

You will inevitably fail along the way. What seemed like good investments will turn into blatantly bad investments. You’ll doubt yourself, and you’ll want to give up. Don’t. Quitting will only guarantee that you won’t achieve your goal. It’s that simple.

Not fully embracing your life as an entrepreneur and investor

There are arguably two viable ways to become a self-made millionaire by 30: investing in the stock market and/or investing in a business idea. Unless you were a kid genius, even if you went to med school right out of college, you probably won’t be able to make millions by the time you’re 30. You have to take on investments or start a business/get involved in multiple business projects. There’s no way around it. Embrace it.

Ending your workday too early

You absolutely have to hustle if you want to become a millionaire. You should plan on working 12 hour days for the next several years to make your financial dreams a reality. This may mean working 8 to 5 at a regular job and then working on side projects/businesses when you get home and on the weekends. You can focus on your work/life balance after you’ve established yourself in a highly successful position.

Neglecting to build your network

If you’re not rubbing elbows with potential business contacts and business partners, you’re going to be on a long, difficult road to financial success. The people in your network can open up some major opportunities for you and jump in on business projects you’re trying to launch. No millionaire is an island, so get out there and meet people.

Setting goals that are too easy

It’s better to aim to make $15 million next year than $1 million. If you only end up earning $1 million, you’ll probably still be satisfied with your progress. The more ambitious your goals, the harder you’ll work, and the more likely you’ll be to succeed. Aiming for the highest income possible is something millionaire Grant Cardone recommends.

Throwing the baby out with the bathwater

If a project fails or you make a bad investment, you have to take what you learned and apply it to future decisions you make. Learning the correct lessons from your failures is key to becoming a financial success. You don’t need to start over every time something doesn’t work out. Move forward instead. For some inspiration, take a look at what some top entrepreneurs learned from their fails.

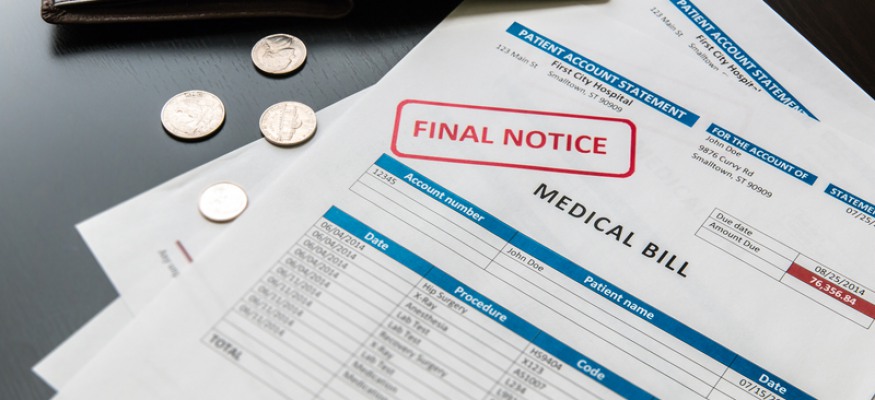

Neglecting debt

Making minimum payments on your credit cards and student loans may have a seemingly positive effect on your cash flow, but it’s going to cause problems down the road. Pay off your debt as soon as you possibly can. It will give you the freedom to take on new, good debt in the form of real estate and business investments. Be sure to check out these innovative ways to pay off student loan debt.

Prioritizing the wrong tasks

If you’re already working 12+ hour days, great. If you’re working long hours and still not increasing your income by much, you’re probably doing something wrong and prioritizing the wrong tasks. Take a good look at how you plan your days out and make sure you’re devoting the most time and energy to tasks that will give you the highest ROI.

{kind=link}